Summary

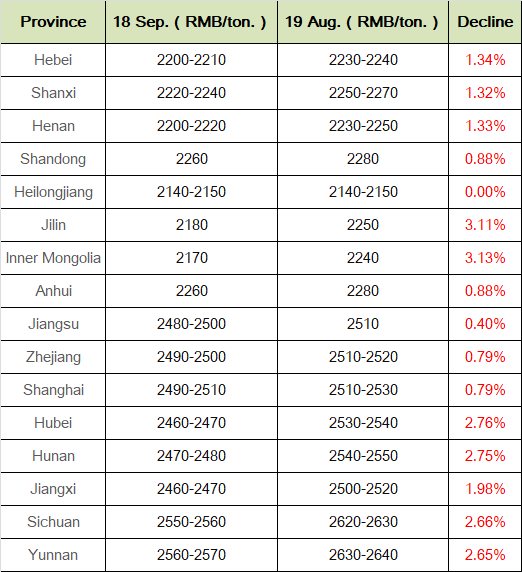

Since August, the auctions of rotation grain by

branches of Sinograin in various places have been very intensive. Since late

August, the transaction rate has been at a relatively high level. Entering

September, the market supply is still loose. The market transaction price has

fallen slightly compared with August. At the same time, downstream enterprises

mainly replenish stocks based on rigid demand. Spot transactions are relatively

sluggish, making corn prices lack upward momentum.

Factors of Price Decline

Influence of weather factors:

Recently, water-soaked corn in Northeast China has been harvested and put

on the market in succession. It has low test weight, high mildew content and

moisture, but it has a relatively obvious price advantage. It continues to flow

into the market for circulation. Under the pressure of repaying tripartite

funds, some trading entities continue to ship. Deep-processing and feed

enterprises have an obvious wait-and-see attitude and mainly consume their own

inventories. The market sentiment is weak and the price is adjusted downward

weakly. In terms of new crops, there is less precipitation and higher

temperature in Northeast production areas, which is conducive to draining

moisture and reducing waterlogging in fields with waterlogging in the early

stage and is beneficial to the formation of corn crop yield.

Influence of inventory factors:

The corn inventory of downstream feed enterprises has increased and the

spot trading volume is low.

In September, the market enters the season of alternating old and new. The

remaining high-quality inventory corn has decreased. At present, the quantity

of fresh corn on the market is still relatively small. The corn inventory of

feed and breeding enterprises in sales areas has gradually increased. In late

August, the corn inventory of large and medium-sized feed enterprises in

southern sales areas was 20-30 days. In early September, the corn inventory of

most enterprises increased to 30-40 days. In the inland market of Central

China, Hubei spring corn was mostly purchased in the early stage. In the South

China market, due to geographical advantages, Northeast corn is mainly

purchased. Generally speaking, the southern sales area market has weak demand

for Northeast spot corn.

Source: China Grain Net.

Future Outlook and Challenges

Supply aspect: Currently, the main holders of grain in corn-producing areas still have a

certain amount of surplus grain. At the same time, new corn in some planting

areas in Northeast and North China has begun to be harvested successively and

is continuously flowing into the market, with supply pressure continuously

rising. For example, new-season corn in Liaoning has been put on the market,

and new-season corn in Heilongjiang region will also be supplied successively

from late September to early October. In addition, Sinograin continuously

releases corn grain sources. Coupled with measures such as rotational grain and

auctions of imported corn, market supply is further increased, making it

difficult to reverse the pattern of supply exceeding demand in the short term.

Impact of expected production reduction: This year, most areas in North China experienced drought in the early

summer, floods in the later period, and rainy weather during the pollination

period. There is a strong expectation of production reduction for corn. Corn in

some low-lying areas in Northeast China also has an expected production

reduction. If the reduction is large, it may alleviate the supply pressure in

the market to a certain extent and provide support for corn prices.

Seasonal changes in demand: With the arrival of the fourth quarter, industries such as pig farming

enter the traditional peak season, and feed demand is expected to increase,

which will have a certain pulling effect on corn prices. However, it is still

necessary to pay attention to the recovery status of the pig farming industry

and the procurement strategies of feed enterprises.

Policy factors: Changes in government agricultural policies, subsidies, tariffs, and

import and export restrictions will also affect corn prices. For example,

government support policies for corn cultivation or regulatory policies for

imported corn may all change the supply and demand pattern of the corn market.

About CCM:

CCM is the leading market intelligence provider for China’s agriculture, chemicals, food & feed and life science markets. Founded in 2001, CCM offers a range of content solutions, from price and trade analysis to industry newsletters and customized market research reports. CCM is a brand of Kcomber Inc.

For more information about CCM, please visit www.cnchemicals.com or get in touch with us directly by emailing econtact@cnchemicals.com or calling +86-20-37616606.